Abstract of the project

Objective:

In this data challenge, I am going to work with 8 datasets from a bank (dataset was collected from year of 1999). Analyze the data and train the model to predict the customers that may default on loans.

Steps:

- Data pre-processing

- Load the data from .asc file into pd.DataFrame data structure.

- Transform the data into the ideal format and content.

- Rename and drop the columns if needed.

- Include some basic feature engineering for each table, such as encoding for categorical features and pivot.

- Analyze the data distribution by visualization.

- Feature Engineering and Dataset Preparation

- Merge some tables to create new features that may relate to the prediction.

- Merge all the tables together to feed to the model. Only in int and float type. Drop or fill the columns with null values.

- Conduct feature selection.

- Baseline model

- Begin with Linear SVM.

- Evaluation

- Visualize the coeff of features.

- Tune hyper-parameters for SVM.

- Try other models

- Random Forest

- AdaBoost

- Gradient Boosting

- XGBoost

- Concolusion

Note: This blog is part 2 of the whole project, only contains the feature engineering and dataset preparation. Please refer to the rest blogs for the following parts.

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set(font_scale = 1.2)

%matplotlib inline

Feature Engineering and Dataset Preparation

Merge loan, account, and transaction tables.

- merge loan and account tables on acount_id

- merge with transaction table with account_id

With the merge function, we can define the key to be merged on, and the way to merge(inner, left, right, outer), we can customize the suffixes of the merged table if there are columns with same name in both tables.

loan_account = pd.merge(loan,

account,

how = 'left',

on = 'account_id',

suffixes = ('_loan','_acc'))

loan_account.head()

|

loan_id |

account_id |

date |

amount |

duration |

payments |

status |

district_id |

frequency |

usage_year |

| 0 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

30 |

1 |

6 |

| 1 |

5316 |

1801 |

1993-07-11 |

165960 |

36 |

4610.0 |

0 |

46 |

2 |

6 |

| 2 |

6863 |

9188 |

1993-07-28 |

127080 |

60 |

2118.0 |

0 |

45 |

2 |

6 |

| 3 |

5325 |

1843 |

1993-08-03 |

105804 |

36 |

2939.0 |

0 |

12 |

2 |

6 |

| 4 |

7240 |

11013 |

1993-09-06 |

274740 |

60 |

4579.0 |

0 |

1 |

1 |

6 |

loan_account_trans = pd.merge(loan_account,

trans,

how = 'left',

on = 'account_id',

suffixes = ('_loan','_trans')

)

# display into two seperate parts just for the tight layout of the blog

display(loan_account_trans.iloc[:2, :11])

display(loan_account_trans.iloc[:2, 11:])

|

loan_id |

account_id |

date |

amount_loan |

duration |

payments |

status |

district_id |

frequency |

usage_year |

trans_id |

| 0 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

30 |

1 |

6 |

523621 |

| 1 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

30 |

1 |

6 |

524054 |

|

trans_date |

type |

operation |

amount_trans |

balance |

k_symbol |

bank |

account |

trans_type |

large_amount |

| 0 |

1993-03-22 |

PRIJEM |

VKLAD |

1100.0 |

1100.0 |

missing |

NaN |

NaN |

1.0 |

1 |

| 1 |

1993-04-21 |

PRIJEM |

VKLAD |

9900.0 |

11000.0 |

missing |

NaN |

NaN |

1.0 |

3 |

Calculate the date difference between loan and transaction

I use the date - transaction date to obtain the date difference between the loan grant date and the transaction date. Filters the records of transactions before loan approval to investigate clients’ financial situation and habbits. This also meets the actual needs: we need to analyze the past transactions to verify whether the client’s loan application can be approved.

- loan_trans_diff:

- greater than 0: indicates the transactions before the loan approval

- less than 0: indicates the transactions after the loan approval

loan_account_trans['loan_trans_diff'] = ((loan_account_trans['date'] - loan_account_trans['trans_date']) / np.timedelta64(1, 'D')).astype(int)

loan_account_trans = loan_account_trans[loan_account_trans['loan_trans_diff'] >= 0]

display(loan_account_trans.iloc[:2, :11])

display(loan_account_trans.iloc[:2, 11:])

|

loan_id |

account_id |

date |

amount_loan |

duration |

payments |

status |

district_id |

frequency |

usage_year |

trans_id |

| 0 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

30 |

1 |

6 |

523621 |

| 1 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

30 |

1 |

6 |

524054 |

|

trans_date |

type |

operation |

amount_trans |

balance |

k_symbol |

bank |

account |

trans_type |

large_amount |

loan_trans_diff |

| 0 |

1993-03-22 |

PRIJEM |

VKLAD |

1100.0 |

1100.0 |

missing |

NaN |

NaN |

1.0 |

1 |

105 |

| 1 |

1993-04-21 |

PRIJEM |

VKLAD |

9900.0 |

11000.0 |

missing |

NaN |

NaN |

1.0 |

3 |

75 |

Average transaction amount over the past period of time: 2 weeks, 1 month, and 3 months before loan date

What was the average transaction amount over the past period of time? Using groupby and aggregation can help us extract this information. The previous average transaction information can obtain the effective characteristics of the customer’s transaction habits. Therefore, these data can be used to determine whether the customer will default on repayment, and then the bank can consider approving or rejecting the loan application.

two_week = loan_account_trans[loan_account_trans['loan_trans_diff'] <= 14]

two_week = two_week.groupby(['loan_id'], as_index = None).mean()

two_week['balance_before_loan_2w'] = two_week['balance']

two_week = two_week.loc[:, ['loan_id', 'balance_before_loan_2w']]

display(two_week.head(5))

|

loan_id |

balance_before_loan_2w |

| 0 |

4959 |

25996.825 |

| 1 |

4962 |

35169.220 |

| 2 |

4967 |

31329.250 |

| 3 |

4968 |

32703.700 |

| 4 |

4973 |

24468.850 |

one_month = loan_account_trans[loan_account_trans['loan_trans_diff'] <= 30]

one_month = one_month.groupby(['loan_id'],as_index = None).mean()

one_month['balance_before_loan_1m'] = one_month['balance']

one_month = one_month.loc[:,['loan_id','balance_before_loan_1m']]

display(one_month.head(5))

|

loan_id |

balance_before_loan_1m |

| 0 |

4959 |

29349.755556 |

| 1 |

4961 |

14062.416667 |

| 2 |

4962 |

60769.460000 |

| 3 |

4967 |

33760.620000 |

| 4 |

4968 |

31890.450000 |

three_month = loan_account_trans[loan_account_trans['loan_trans_diff'] <= 90]

three_month = three_month.groupby(['loan_id'],as_index = None).mean()

three_month['balance_before_loan_3m'] = three_month['balance']

three_month = three_month.loc[:,['loan_id','balance_before_loan_3m']]

display(three_month.head(5))

|

loan_id |

balance_before_loan_3m |

| 0 |

4959 |

29830.005000 |

| 1 |

4961 |

15123.228571 |

| 2 |

4962 |

67547.706897 |

| 3 |

4967 |

20759.711111 |

| 4 |

4968 |

26212.342308 |

Transaction frequence

before = loan_account_trans

before['trans_year'] = before['trans_date'].dt.year # extract the year from datetime column

before.head(2)

|

loan_id |

account_id |

date |

amount_loan |

duration |

payments |

status |

district_id |

frequency |

usage_year |

... |

operation |

amount_trans |

balance |

k_symbol |

bank |

account |

trans_type |

large_amount |

loan_trans_diff |

trans_year |

| 0 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

30 |

1 |

6 |

... |

VKLAD |

1100.0 |

1100.0 |

missing |

NaN |

NaN |

1.0 |

1 |

105 |

1993 |

| 1 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

30 |

1 |

6 |

... |

VKLAD |

9900.0 |

11000.0 |

missing |

NaN |

NaN |

1.0 |

3 |

75 |

1993 |

2 rows × 23 columns

groupby loan id and the year of transaction date

trans_freq = before.loc[:, ['loan_id','trans_year','balance']].groupby(['loan_id','trans_year']).count()

trans_freq.rename(columns={'balance':'trans_freq'}, inplace = True)

trans_freq.head()

|

|

trans_freq |

| loan_id |

trans_year |

|

| 4959 |

1993 |

54 |

| 1994 |

1 |

| 4961 |

1995 |

54 |

| 1996 |

26 |

| 4962 |

1996 |

46 |

f = {'trans_freq': ['sum', 'mean'],

'trans_year': ['count']}

trans_freq = trans_freq.reset_index().groupby('loan_id').agg(f)

trans_freq.columns = [s1 + '_' + s2 for (s1,s2) in trans_freq.columns.to_list()]

trans_freq.reset_index(inplace = True)

Number of large amount transactions

We encoded the transaction amount by quantile. If the transaction amount greater than Q3, then it is encoded to 3.

large_amount = before[before['large_amount'] == 3]

large_amount_freq = large_amount.loc[:,['loan_id','large_amount']].groupby(['loan_id']).count()

large_amount_freq.rename(columns = {'large_amount': 'large_amount_freq'}, inplace = True)

display(large_amount_freq.head())

|

large_amount_freq |

| loan_id |

|

| 4959 |

24 |

| 4961 |

26 |

| 4962 |

83 |

| 4967 |

32 |

| 4968 |

16 |

Number of transactions when balance lower than 5k

low_5k = before[before['balance'] <= 5000]

low_5k_freq = low_5k.loc[:,['loan_id', 'balance']].groupby(['loan_id']).count()

low_5k_freq.rename(columns = {'balance': 'low_5k_freq'},inplace = True)

display(low_5k_freq.head())

|

low_5k_freq |

| loan_id |

|

| 4959 |

1 |

| 4961 |

10 |

| 4962 |

1 |

| 4967 |

3 |

| 4973 |

1 |

Combine engineered features (transaction habbits)

loan_info = loan.merge(three_month,

how = 'left',

on = 'loan_id')

loan_info = loan_info.merge(two_week,

how = 'left',

on = 'loan_id')

loan_info = loan_info.merge(one_month,

how = 'left',

on = 'loan_id')

loan_info = loan_info.merge(trans_freq,

how = 'left',

on = 'loan_id')

loan_info = loan_info.merge(large_amount_freq,

how = 'left',

on = 'loan_id')

loan_info = loan_info.merge(low_5k_freq,

how = 'left',

on = 'loan_id')

loan_info.head()

|

loan_id |

account_id |

date |

amount |

duration |

payments |

status |

balance_before_loan_3m |

balance_before_loan_2w |

balance_before_loan_1m |

trans_freq_sum |

trans_freq_mean |

trans_year_count |

large_amount_freq |

low_5k_freq |

| 0 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

15966.666667 |

NaN |

20100.000000 |

4 |

4.0 |

1 |

1.0 |

1.0 |

| 1 |

5316 |

1801 |

1993-07-11 |

165960 |

36 |

4610.0 |

0 |

56036.575862 |

36072.350000 |

33113.788889 |

37 |

37.0 |

1 |

14.0 |

2.0 |

| 2 |

6863 |

9188 |

1993-07-28 |

127080 |

60 |

2118.0 |

0 |

35160.929412 |

20272.800000 |

36233.066667 |

24 |

24.0 |

1 |

9.0 |

1.0 |

| 3 |

5325 |

1843 |

1993-08-03 |

105804 |

36 |

2939.0 |

0 |

46378.637500 |

34243.066667 |

42535.133333 |

25 |

25.0 |

1 |

13.0 |

1.0 |

| 4 |

7240 |

11013 |

1993-09-06 |

274740 |

60 |

4579.0 |

0 |

60804.547059 |

41127.900000 |

49872.757143 |

27 |

27.0 |

1 |

16.0 |

1.0 |

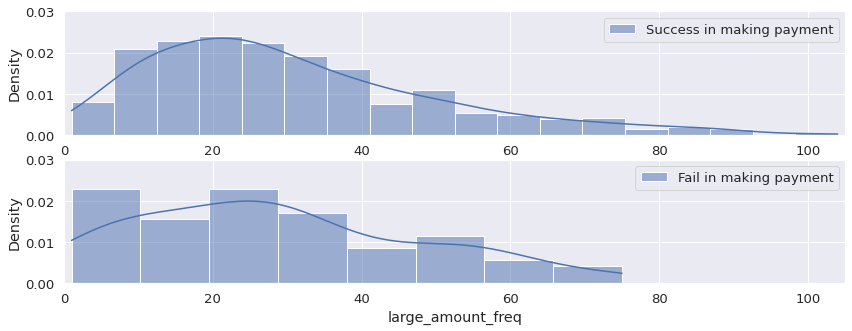

Compare two types of clients:

- status = 0: successfully make payments

- status = 1: fail to make payments

I observe their habits of large-amount transactions.

loan_info[loan_info['status'] == 0]['large_amount_freq'].describe()

count 605.000000

mean 30.737190

std 19.470525

min 1.000000

25% 16.000000

50% 26.000000

75% 41.000000

max 104.000000

Name: large_amount_freq, dtype: float64

loan_info[loan_info['status'] == 1]['large_amount_freq'].describe()

count 76.000000

mean 28.723684

std 19.039327

min 1.000000

25% 13.750000

50% 26.000000

75% 42.250000

max 75.000000

Name: large_amount_freq, dtype: float64

# making subplots to compare the payment habbits of these two types of clients

plt.figure(figsize = (14, 5))

plt.subplot(211)

sns.histplot(loan_info[loan_info['status'] == 0]['large_amount_freq'],

stat = 'density', kde = True,

label = 'Success in making payment')

plt.legend()

plt.ylim(0, 0.03)

plt.xlim(0, 105)

plt.subplot(212)

sns.histplot(loan_info[loan_info['status'] == 1]['large_amount_freq'],

stat = 'density', kde = True,

label = 'Fail in making payment')

plt.ylim(0, 0.03)

plt.xlim(0, 105)

plt.legend()

Merge all tables

data = pd.merge(loan_info,

account,

how = 'left',

on = 'account_id'

)

data = pd.merge(data,

disp,

how = 'left',

on = 'account_id'

)

data = pd.merge(data,

card,

how = 'left',

on = 'disp_id'

)

data = pd.merge(data,

order,

how = 'left',

on = 'account_id'

)

data = pd.merge(data,

client,

how = 'left',

on = 'client_id'

)

data = pd.merge(data,

district,

how = 'left',

left_on = 'district_id_x',

right_on = 'A1'

)

display(data.iloc[:3, :10])

display(data.iloc[:3, 10: 21])

display(data.iloc[:3, 21: 30])

display(data.iloc[:3, 30:])

|

loan_id |

account_id |

date |

amount_x |

duration |

payments |

status |

balance_before_loan_3m |

balance_before_loan_2w |

balance_before_loan_1m |

| 0 |

5314 |

1787 |

1993-07-05 |

96396 |

12 |

8033.0 |

1 |

15966.666667 |

NaN |

20100.000000 |

| 1 |

5316 |

1801 |

1993-07-11 |

165960 |

36 |

4610.0 |

0 |

56036.575862 |

36072.35 |

33113.788889 |

| 2 |

6863 |

9188 |

1993-07-28 |

127080 |

60 |

2118.0 |

0 |

35160.929412 |

20272.80 |

36233.066667 |

|

trans_freq_sum |

trans_freq_mean |

trans_year_count |

large_amount_freq |

low_5k_freq |

district_id_x |

frequency |

usage_year |

disp_id |

client_id |

card_id |

| 0 |

4 |

4.0 |

1 |

1.0 |

1.0 |

30 |

1 |

6 |

2166 |

2166 |

NaN |

| 1 |

37 |

37.0 |

1 |

14.0 |

2.0 |

46 |

2 |

6 |

2181 |

2181 |

NaN |

| 2 |

24 |

24.0 |

1 |

9.0 |

1.0 |

45 |

2 |

6 |

11006 |

11314 |

NaN |

|

type |

issued |

amount_y |

order_a_k_LEASING |

order_a_k_Missing_symbol |

order_a_k_POJISTNE |

order_a_k_SIPO |

order_a_k_UVER |

birth_number |

| 0 |

NaN |

NaN |

8033.2 |

0.0 |

0.0 |

0.0 |

0.0 |

8033.2 |

475722 |

| 1 |

NaN |

NaN |

13152.0 |

0.0 |

3419.0 |

956.0 |

4167.0 |

4610.0 |

680722 |

| 2 |

NaN |

NaN |

10591.3 |

0.0 |

471.0 |

66.0 |

7936.0 |

2118.3 |

360602 |

|

district_id_y |

sex |

age |

A1 |

A4 |

A5 |

A6 |

A7 |

A8 |

A9 |

A10 |

A11 |

A12 |

A13 |

A14 |

A15 |

A16 |

| 0 |

30 |

1 |

52 |

30 |

94812 |

15 |

13 |

8 |

2 |

10 |

81.8 |

9650 |

3.38 |

3.67 |

100 |

2985 |

2804 |

| 1 |

46 |

0 |

31 |

46 |

112709 |

48 |

20 |

7 |

3 |

10 |

73.5 |

8369 |

1.79 |

2.31 |

117 |

2854 |

2618 |

| 2 |

45 |

0 |

63 |

45 |

77917 |

85 |

19 |

6 |

1 |

5 |

53.5 |

8390 |

2.28 |

2.89 |

132 |

2080 |

2122 |

data['year'] = data['date'].dt.year

data['year_loan'] = 1999 - (data['year']).astype(int)

Drop unnecessary columns

data.drop(['date','year', 'account_id', 'birth_number', 'card_id',

'client_id', 'disp_id', 'district_id_x', 'district_id_y','issued',

'loan_id', 'A12', 'A15'], axis = 1, inplace = True)

Index(['amount_x', 'duration', 'payments', 'status', 'balance_before_loan_3m',

'balance_before_loan_2w', 'balance_before_loan_1m', 'trans_freq_sum',

'trans_freq_mean', 'trans_year_count', 'large_amount_freq',

'low_5k_freq', 'frequency', 'usage_year', 'type', 'amount_y',

'order_a_k_LEASING', 'order_a_k_Missing_symbol', 'order_a_k_POJISTNE',

'order_a_k_SIPO', 'order_a_k_UVER', 'sex', 'age', 'A1', 'A4', 'A5',

'A6', 'A7', 'A8', 'A9', 'A10', 'A11', 'A13', 'A14', 'A16', 'year_loan'],

dtype='object')

data['type'].fillna(-1, inplace = True)

data.fillna(0, inplace = True)

data.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 682 entries, 0 to 681

Data columns (total 36 columns):

amount_x 682 non-null int64

duration 682 non-null int64

payments 682 non-null float64

status 682 non-null int64

balance_before_loan_3m 682 non-null float64

balance_before_loan_2w 682 non-null float64

balance_before_loan_1m 682 non-null float64

trans_freq_sum 682 non-null int64

trans_freq_mean 682 non-null float64

trans_year_count 682 non-null int64

large_amount_freq 682 non-null float64

low_5k_freq 682 non-null float64

frequency 682 non-null int64

usage_year 682 non-null int64

type 682 non-null float64

amount_y 682 non-null float64

order_a_k_LEASING 682 non-null float64

order_a_k_Missing_symbol 682 non-null float64

order_a_k_POJISTNE 682 non-null float64

order_a_k_SIPO 682 non-null float64

order_a_k_UVER 682 non-null float64

sex 682 non-null int64

age 682 non-null int64

A1 682 non-null int64

A4 682 non-null int64

A5 682 non-null int64

A6 682 non-null int64

A7 682 non-null int64

A8 682 non-null int64

A9 682 non-null int64

A10 682 non-null float64

A11 682 non-null int64

A13 682 non-null float64

A14 682 non-null int64

A16 682 non-null int64

year_loan 682 non-null int64

dtypes: float64(16), int64(20)

memory usage: 197.1 KB

- the input are features

- the output should be the status: 0 / 1

I split train and test with a ratio of 2:1

from sklearn.model_selection import train_test_split

X = data.loc[:, data.columns != 'status']

y = data['status']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size = 1/3)

len(X_train), len(X_test)